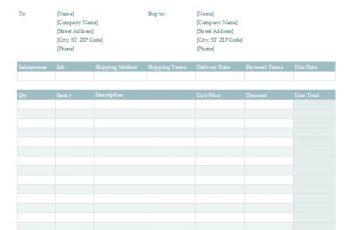

Sales Order Template: Free Download, Edit, Fill, Create and Print By : pdf.wondershare.com … Sales Order Template

blank check register Kleo.beachfix.co By : kleo.beachfix.co Go to the Exchange tab and … Blank Check Register Pdf

free employee schedule template schedule sheet free passionativeco By : gtsak.info Closely linked … Free Employee Work Schedules

Daily Cash Report Template By : www.bizmanualz.com In today’s data-driven culture where you … End Of Day Cash Register Report Template

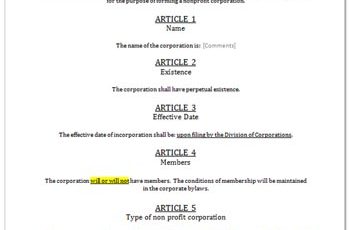

Articles of Incorporation – Free Sample Template Form By : www.northwestregisteredagent.com If your … Free Articles Of Incorporation

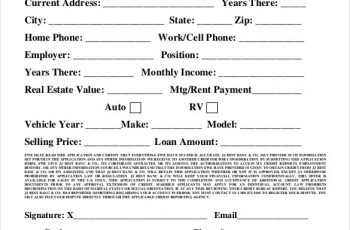

Auto Loan Credit Application Form Pdf Auto Loan Application Form By : www.pinterest.com … Auto Credit Application Pdf

Printable Medical Sign In Sheet By : www.freeprintablemedicalforms.com Several teachers scream in the … Medical Sign In Sheets

expense tracker printable April.onthemarch.co By : april.onthemarch.co Cost Tracker Easily establish in addition … Expense Tracker Printable